At least 70% of listed organisations use relative TSR as a performance measure under long term incentive (LTI) programs.

Yet the assessment and verification of employee entitlements under such plans can lead to unexpected complexity.

Egan Associates’ analytics function supports clients in this arena, performing benchmark analysis on relative TSR to determine the percentage of rights which vest and verify Board and/or Remuneration Committee’s decisions to vest securities. We also monitor relative TSR performance over a series of grants on a six monthly basis as requested by clients to inform the Board, Remuneration Committee and key executives how performance is tracking against TSR hurdles.

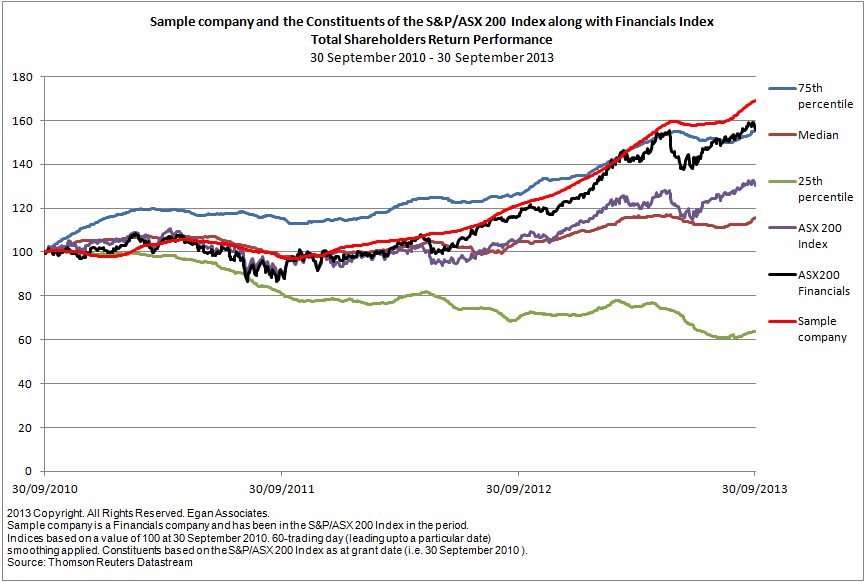

Click to enlarge

In the last decade of undertaking analytical work and providing recommendations for ASX listed organisations (although an increasing proportion of our analysis involves international comparators), we have noticed significant variations in the methods and assumptions used to calculate entitlements. Some of these variants are industry specific while some of them are organisation specific.

The issues that Egan Associates has observed that have become increasingly relevant and are creating some confusion are:

- Does the company benchmark its performance against an index? Which index should it select? Should this be an industry specific index or rank specific index? Should the index exclude some industries or organisations?

- Is the industry sector comparator group the most relevant given the significant variability in market capitalisation of its constituents, e.g. $500 Million to over $5 Billion?

- Does smoothing address market variability? Over what period should the data be smoothed?

- Should retesting be applied? Should it be regular or one-off? Is it daily, quarterly, six monthly or annually?

- For an international multi-currency comparator benchmark, should performance be indexed to a single currency?

- How should the dynamics of the comparator group be treated; eg companies delisting, moving in or out of the index, demerging, divesting significant assets/businesses?

- How does market speculation impact certain organisations, eg news of a takeover, merger, government investigation, international shareholding approvals, the grant of an export license? How should this be considered in the analysis?

Over the next 6 months, we will illustrate these issues by way of a series of case studies. This series will focus entirely on performance management and not on securities valuation.